What do you think?

Rate this book

496 pages, Hardcover

First published March 18, 2025

Markets are more or less efficient, except when they’re not. [p. 328]

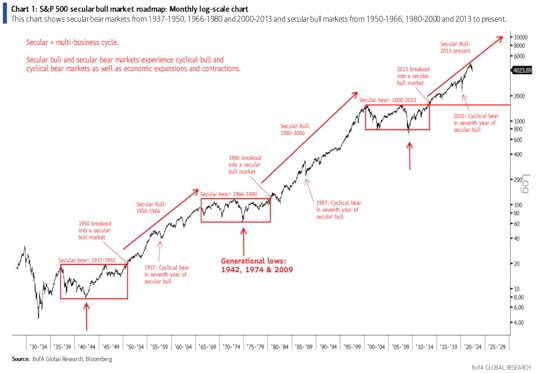

It’s almost as if your portfolio compounds over time regardless of the news....This is essentially a book on behavioral finance. The focus is not on the nuts and bolts of how to invest, but rather a concentration on people's behavior when they interact with money; how financial desire impacts our decision-making abilities; what risks we embrace, how we think about wealth.

[E]ven when events of great geopolitical significance occur, markets tend to shudder, then go back to whatever they were doing before.

You should have an investment philosophy that can be expressed in a portfolio. This philosophy should include specific rules that you do not ignore. You want a portfolio with low costs, low turnover, low taxes and a long holding period.While most of the advice is sound (albeit also mostly obvious), I disagree with his argument in support of indexing. Indexing is a perfectly valid strategy, and pretty much locks a passive investor into the bounty of realizing market returns. It is the approach of choice for many, many investors. However, Ritholtz bases his argument for it on this paper by Bessembinder et al. [Hendrik Bessembinder, Te-Feng Chen, Goeun Choi and John Wei, “Do Global Stocks Outperform US Treasury Bills?” ssrn.com (July 9, 2019).] which shows that just 1.3% of the best performing stocks account for all of the equity market's excess returns above Treasury bills. Ritholtz argues that with such a low percentage of high performing stocks, you need to buy the entire market (through index funds) to ensure you are getting the winners. Sort of feels like he is falling prey to the Denominator Blindness he warns about earlier in the book. I would argue that you are just guaranteeing to yourself that you will get a huge bunch of low performing stocks. Their analysis included 17,310 US stocks. So the 1.3% referenced above includes 225 stocks. While no stock picker is going to pick only the high flyers, it seems pretty straight-forward to use the "what makes a good company" principles elaborated by the likes of Ben Graham, Phil Fisher, Warren Buffett, etc. to eliminate many, many of the bottom feeders in this 17,310 stock list. Why would you want those in your portfolio? In fact, at another point in the book, he makes this same case: "Managers should consider focusing less on being stock pickers, and more on being “stock-unpickers”—in other words, avoiding the dogs."